For HNW investors, a well-structured municipal bond portfolio helps balance income, flexibility, and risk management in a tax-efficient way.

High-net-worth (HNW) portfolios often have two core objectives: tax-efficient income and capital preservation. Municipal bonds (munis) are a way to address both, offering tax-exempt interest that is especially valuable for investors in higher tax brackets. To enhance outcomes when incorporating munis into a client’s financial plan, some advisors recommend using separately managed accounts (SMAs) to tailor portfolios, enabling the optimization of yield curve exposure, efficient tax lot management, issuer-specific customization, and pre-transition risk analysis through advanced portfolio analytics tools.

If this is a path you are considering, there are three factors to keep in mind:

- Structure

- After-tax income

- Research and diversification

Structure matters: Blend for stability and opportunity

For HNW clients, a well-structured municipal bond portfolio helps balance income, flexibility, and risk management. It’s our role as an advisor to help get that structure right. A common starting point is a laddered SMA with maturities ranging from 1 to 10 years, which can deliver steady income and predictable cash flows while managing interest rate risk. Many HNW investors also may benefit from hybrid portfolios (e.g., combining 80% individual bonds with 20% municipal bond mutual funds or exchange-traded funds) to maintain customization while adding tactical flexibility. No matter the blend, the duration strategy should align with both the client’s liquidity needs and the advisor's view on interest rates.

Munis still deliver compelling after-tax income

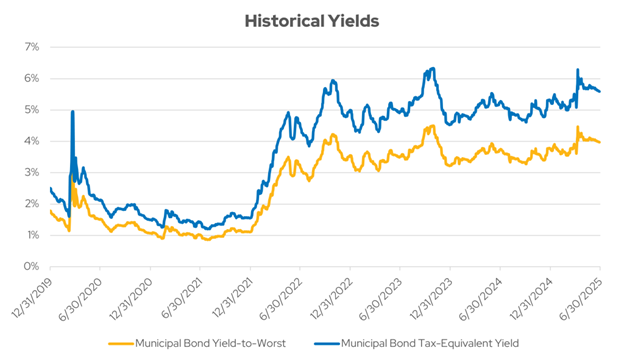

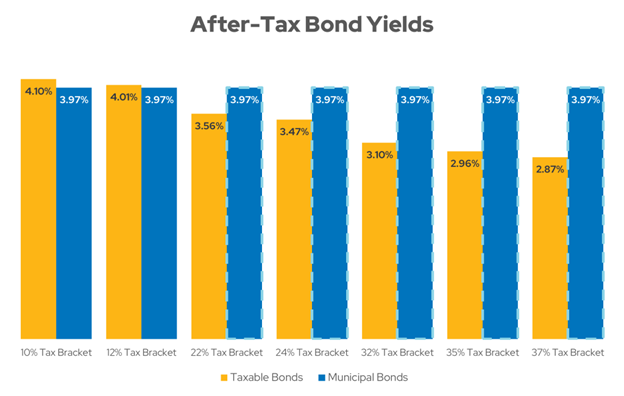

Municipal bonds continue to offer compelling after-tax income, making them especially attractive for HNW clients in higher tax brackets. When you factor in tax-equivalent yields, munis often outperform comparable taxable fixed income options, reinforcing their role as a core income-generating asset. For example, a 4% yield on a tax-exempt municipal bond can be equivalent to a 6.5% taxable yield for a client in the top federal tax bracket, making the muni a clear winner on an after-tax basis.

Source: Bloomberg data through 6/30/25.

Source: Bloomberg data through 6/30/25.

For clients seeking even greater yield, high-yield municipal bonds can be a logical addition. While they do carry slightly more credit risk, defaults in this space have historically been rare. A well-diversified allocation to high-yield munis — say 10–15% of the total portfolio — can have the potential to enhance income without taking on excessive risk.

Research and diversification drive quality outcomes

Strong municipal bond portfolios don’t happen by accident. They’re built through rigorous research and thoughtful diversification. Portfolios benefit from deep credit analysis and active oversight, with advisors and managers carefully selecting issuers, monitoring sector exposure, and rotating risk as conditions change. For example, if a client's portfolio is overweight in hospital revenue bonds, reallocating some exposure to general obligation or essential service bonds can help reduce concentration risk. Diversifying by credit rating, geography, and issuer type further helps manage both credit and liquidity risk while supporting consistent performance.

This kind of strategic construction not only enhances long-term resilience but also reinforces your value as an advisor who understands how to protect and grow wealth through disciplined fixed income management. An experienced advisor, often working with an asset manager, brings the judgment needed to evaluate relative value, navigate evolving tax considerations, and align municipal bond strategies with a client’s broader financial goals. Deep research and customization deliver a level of insight and accountability that automated platforms can’t replicate.

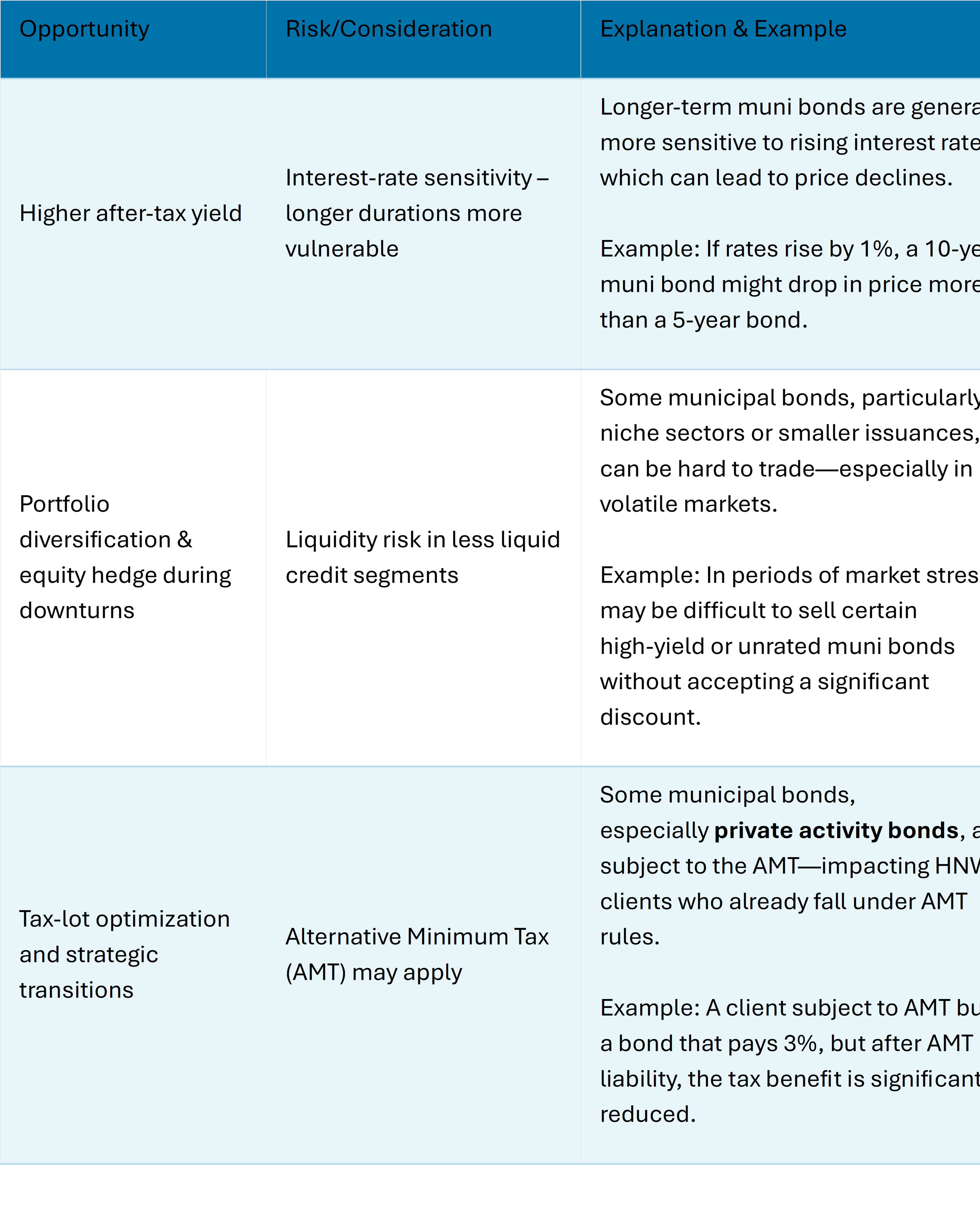

Allocation benefits & risks to consider

As you consider municipal bonds, here are just some of the opportunities and risks you’ll need to balance.

Put it all together for your HNW investors

For HNW clients, a thoughtful municipal bond strategy often begins with a core intermediate municipal separately managed account (SMA), typically with a duration of approximately 2–8 years. This provides a strong foundation for yield, tax efficiency, and capital preservation. For those seeking greater income and willing to assume more risk, layering in high-yield municipal bonds or opportunistic vehicles can enhance return potential. Investors who want their portfolios to reflect their values can also incorporate impact or ESG-focused municipal funds, though it’s important to monitor credit quality and structural nuances.

Munis still matter

Munis can form a powerful core of HNW portfolios. They deliver tax-efficient income, diversification, customization, and access to a deep bond supply.

***DISCLOSURES***

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

Municipal bonds are subject to availability and change in price. They are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply. If sold prior to maturity, capital gains tax could apply.